Products

Products

Ready to get started?

No matter where you are on your CMS journey, we're here to help. Want more info or to see Glide Publishing Platform in action? We got you.

Book a demoAI companies are racing to go public while also raising costs to consumers. Both events put content owners in a squeeze which needs action and decision.

The imaginary tills are ringing, but the money is only going out.

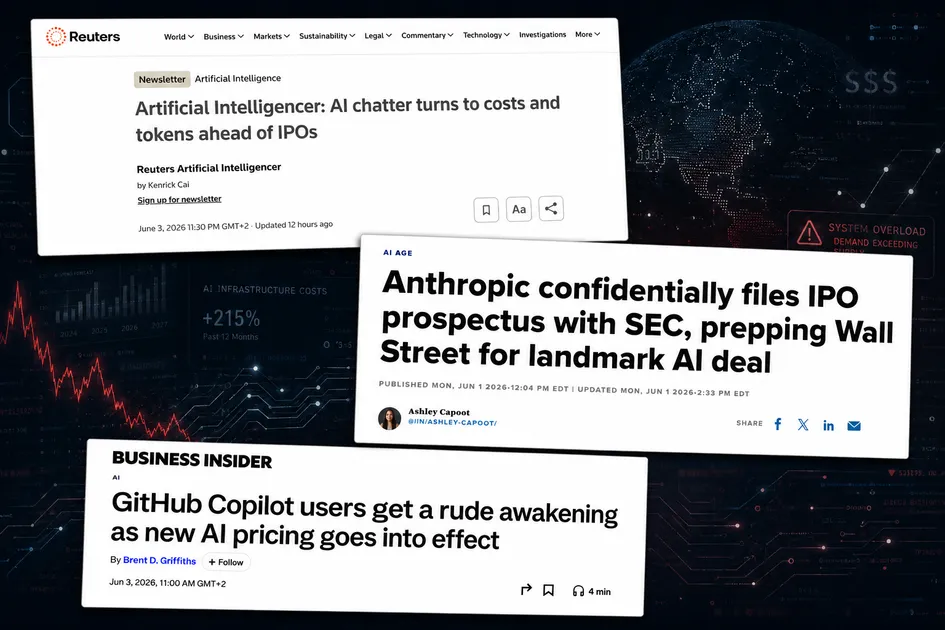

On Monday, Anthropic started the filing process for a $65 billion funding round, against a $965 billion total valuation, just a few days after OpenAI began the process for its own IPO in September against a $1 trillion valuation.

On the same day, Alphabet announced plans to raise $80 billion via stock issues to bolster its AI infrastructure, predicting around $180bn in total AI infrastructure spend this year alone, a number conveniently similar to the $190bn Microsoft has previously committed to capital expenditures for 2026 to feed its thirst for AI capacity.

Three gargantuan financial events arriving almost on top of each other. That's either a coincidence, or a signal. For me, it’s a very loud signal, which publishers should be alert to.

The obvious question is why everyone needs money at the same time. And, when those ringing tills will start taking money in.

AI spending has entered territory without historical precedent. The four largest hyperscalers - Amazon, Microsoft, Alphabet, and Meta - are on track to spend some $725 billion on capital expenditure in 2026. That's up more than 75% from last year.

If you include other large firms and sovereign funds, according to Gartner that $725bn total will double to around $1.44 trillion, blowing through the $1tn mark for the first time and putting AI spend on comparative par with multinational and multidecade endeavours such as the railways, the space race, and the internet.

That’s more than a hole on a balance sheet. It’s a cavern, and it somehow needs filling.

So what do the income lines look like for these giant brands?

Amazon spent $44.2 billion in Q1 of 2026, more than its $37.6 billion revenue from AWS in the same period, while Amazon's free cash flow - which funds the juicy morsels it can give back to investors as dividends - tanked 95% year-on-year, from $26 billion to $1.2 billion. Meanwhile OpenAI is projecting $14 billion in losses this year, with profitability not expected until 2029. Microsoft's AI revenue is on track to be $37 billion for 2026, but its capex is five times that.

These are numbers that private funding cannot sustain, even at record levels. OpenAI raised $122 billion privately, the largest venture round in history, and still needs vastly more. So the money has to come from somewhere new: public markets, institutional investors, and retail investors, for which its IPO will be the mechanism.

To put this in perspective, the entire global news publishing industry is worth around $125 billion annually. That is less than what Microsoft alone plans to spend on AI infrastructure this year. The AI industry is on track to burn through the equivalent of the entire global news publishing economy every 4.5 weeks, and it hasn't worked out how to make that money back yet.

For publishers and media companies - and everyone, in fact - this matters for two immediate reasons.

We've seen this film before. Uber lost $33 billion subsidising rides to build market share, losing 41 cents on every dollar it brought in. Once investors demanded profitability, prices rose 18% per year, nearly four times inflation. Riders who'd built their routines around cheap fares found themselves paying double. The product was the same, but the subsidy was gone.

AI tooling is following the same arc, but at a spending scale which dwarfs Uber’s. For developers doing coding, GitHub Copilot switched to token-based billing this week, which saw developers report bills jumping up to 50-fold overnight. Google added hard spending caps to its Gemini API after customers received surprise bills in the tens of thousands. Anthropic restructured its credit system, AWS is sunsetting its Amazon Q Developer product and pushing users toward Kiro Pro, with the same cost rises pattern emerging.

We can predict that every AI tool currently offered at a flat rate or with generous free credits will follow, and that we're about to find out what the real price of AI is.

Before an IPO, unresolved copyright claims become liabilities in a prospectus. AI companies want clean narratives for Wall Street, which means this moment is of maximum negotiating leverage for content owners.

The New York Times has spent $20 million fighting OpenAI, and Publisher A.G. Sulzberger said this week to a packed auditorium at the World News Congress (WNC) in Marseille that less than 0.5% of $350 billion in private AI investment is going to content creators. He made a brilliant and impassioned speech about the place of news and content in the AI world.

After the IPO, the incentive to do deals and reach agreements reverses. Pre-IPO companies optimise for growth and share, but post-IPO companies optimise for margin. Content licensing becomes a cost to minimise on quarterly earnings calls, and the deals being signed today - such as News Corp at $50 million a year, various publishers licensing via Snowflake's RAG pipeline, Reddit’s $200 million - may well be the best such deals terms ever seen.

There are emerging mechanisms worth watching. Also at WNC in Marseille, Microsoft spoke more of its Publisher Content Marketplace, a clearing house where media owners set licensing terms and AI builders pay based on what they use. Whether it brings revenue at scale to media firms remains to be seen, but it’s an attempt to fix the compensation problem systematically rather than leaving it to lawsuits and ad-hoc deals.

Amazon too is exploring such a marketplace for content. Will they work? Well, I am reminded of how music piracy was mostly solved by simply making it easier and more convenient to stream it from legal sources. Rather than open themselves to constant ongoing litigation, the “good” AIs will eventually settle into being your subscribers.

The likely outcome will still be a two-tier system though. Large publishers with legal resources will lock in direct deals, while everyone else may find marketplaces and collective licensing frameworks are the most realistic path to income from an AI for content.

Either way, now is the time to act before the current giants of AI go public and see content licensing only as a cost line to reduce.

Publishers and media teams therefore face a double squeeze. The AI tools they count on to help them be more efficient are about to get much more expensive, just as their leverage to demand payment is about to diminish.

Two things, and they address different sides of the business.

The first is simple: Act now.

The pre-IPO window is finite, and once these companies are public, the dynamics shift against you. If you're a large publisher with legal resources, pursue direct licensing negotiations before the filings reach the market stage. You have the catalogue depth, the brand recognition, and the legal budget to negotiate something worthwhile. The precedents set now will define what the rest of the industry can expect later, so there's a collective responsibility here too.

If you're a mid-size or smaller publishing brand, direct negotiation with trillion-dollar companies is unrealistic, however your path is equally urgent. Register with emerging licensing mechanisms: Microsoft's Publisher Content Marketplace, Snowflake's Cortex programme, and whatever collective frameworks your industry body is assembling.

At the WNC in Marseille, news body WAN-IFRA alongside David Buttle and Dominic Young revealed rapid growth in the industry initiative SPUR, the Standards for Publishers Usage Rights - a rights and action collective against AI theft of content. Please investigate joining. (I am very pleased to say David Buttle will be a speaker at the Glide Live: London event later this month, so if attending do seek him out.)

Even if you question their efficacy, any of your robots.txt and crawler policies should reflect a deliberate commercial position rather than a default open door. Understand what's being scraped, by whom, and at what volume. The marketplace model, where publishers set terms and AI builders pay on usage, may deliver modest revenue individually, but collectively it establishes the norm that content has a price.

Passivity is the worst option. Every month you wait, your leverage diminishes and the precedents set become the ceiling everyone else inherits. And budget realistically: AI licensing revenue is unlikely to replace what's being lost to AI-powered search and reduced referral traffic. Think of it as a new, supplementary revenue line that needs infrastructure and attention, not a windfall that will arrive without effort.

To my friends at sports organisations and rights holders: this applies to you too. Football clubs, federations, and sporting bodies have long understood that brand IP is a primary commercial lever. You protect broadcast rights, image rights, and sponsorship assets with vigour. The content on your digital platforms is being scraped and ingested by AI models and while it may not be top of the agenda today, it should be on the radar.

The same pre-IPO leverage window exists for rights holders as it does for publishers, and the organisations best placed to act are those who already have the legal infrastructure for IP protection. Treating your digital content estate as an extension of your broader rights portfolio is a natural next step.

Second: design your technology stack for pricing volatility.

Whether you're building your own AI integrations or buying them off the shelf, the principle is the same: design for optionality. Any AI capability you adopt should be something you can dial up, dial down, or turn off entirely without breaking your publishing operation.

That means treating AI as a layer in your workflow, not a foundation. Things like auto-tagging, content recommendations, article linking, image generation, RAG-powered knowledge retrieval, MCP integrations for programmatic workflows all add genuine value, but avoid making them something your team cannot publish without. Don’t turn an external pricing decision into an operational dependency.

Once subsidised pricing disappears, a reassessment is inevitable. Some AI-powered features will prove their ROI at full cost by being so good in comparison to how it is currently done, or the downside of not doing them at all, such as auto-tagging millions of articles from a 20-year archive.

But other trivial uses of AI probably won't justify higher spend once real token costs are visible. The publishers who retain the ability to make that assessment, feature by feature, workflow by workflow, are the ones who'll manage the transition without pain. The ones who baked AI into every operation as a hard dependency will discover they have little room to adjust.

This is certainly how we think about it at Glide and have been saying since the start don’t allow AI to become the central plank in your process. We've gone deep on AI tooling: auto-tagging, auto-linking, article and image recommendations, text-to-speech, drafting, RAG, and MCP server integrations for programmatic AI workflows. But nothing in our platform requires AI to function.

A team can go fully AI-assisted, entirely manual, or anywhere in between, and adjust the balance as costs and utility change. We built it this way because we've been in publishing technology long enough to know that the price you pay today is never the price you pay next year.

The trillion-dollar AI spending cycle is going to change pricing for everyone downstream. The publishers who'll handle it best are the ones who built optionality into their operations before the bill arrived, not after.

No matter where you are on your CMS journey, we're here to help. Want more info or to see Glide Publishing Platform in action? We got you.

Book a demo